Navigating the world of self-employment is an exhilarating journey filled with autonomy and opportunity. As you carve your path and shape your destiny, there’s a multitude of responsibilities that come with the territory. Amidst the hustle and bustle of entrepreneurial endeavors, there’s one aspect that often lingers in the background: life insurance.

While the idea of insurance might not spark immediate excitement, its significance for self-employed individuals cannot be overstated. Imagine it as a safety net, a shield of financial security that safeguards your loved ones and the hard-earned fruits of your labor.

In this complete guide to life insurance for self-employed, we’ll unravel the importance, demystify the options available, and empower you to make informed decisions. Let’s explore together how to secure your future while navigating the unique landscape of self-employment.

Yes, self-employed individuals should strongly consider purchasing life insurance. While it’s not mandatory, securing life insurance is a prudent step towards protecting oneself and loved ones from unforeseen circumstances. Unlike those in traditional employment who might have life insurance coverage through their employers, self-employed individuals bear the responsibility of arranging their own financial protection.

Life insurance serves as a crucial safety net for the self-employed, providing a financial cushion for their families in the event of an untimely death. It can cover various expenses such as outstanding debts, mortgages, funeral costs, and the continuation of living standards for dependents. By having life insurance, self-employed individuals can ensure that their loved ones are taken care of and that their financial obligations are met even in their absence.

Life insurance holds significant importance for self-employed individuals due to several key reasons:

Self-employed individuals often do not have the safety net of employer-provided life insurance. Life insurance ensures that in the unfortunate event of the policyholder’s passing, their dependents are financially supported. It can cover daily living expenses, outstanding debts, mortgage payments, and even future education expenses for children.

For self-employed individuals running businesses, life insurance can be crucial for business continuity. It can help cover business debts, facilitate the transfer of ownership, or provide funds to sustain the business during a difficult transition period.

Knowing that loved ones will be taken care of in the event of an unexpected tragedy can provide immense peace of mind. Life insurance offers reassurance that financial stability and security will be maintained, alleviating worries about the future.

Life insurance can cover funeral costs and other end-of-life expenses, relieving the financial burden on surviving family members during a difficult time.

In essence, life insurance serves as a safety net, offering financial security and stability to self-employed individuals and their families, ensuring they are prepared for any unforeseen circumstances.

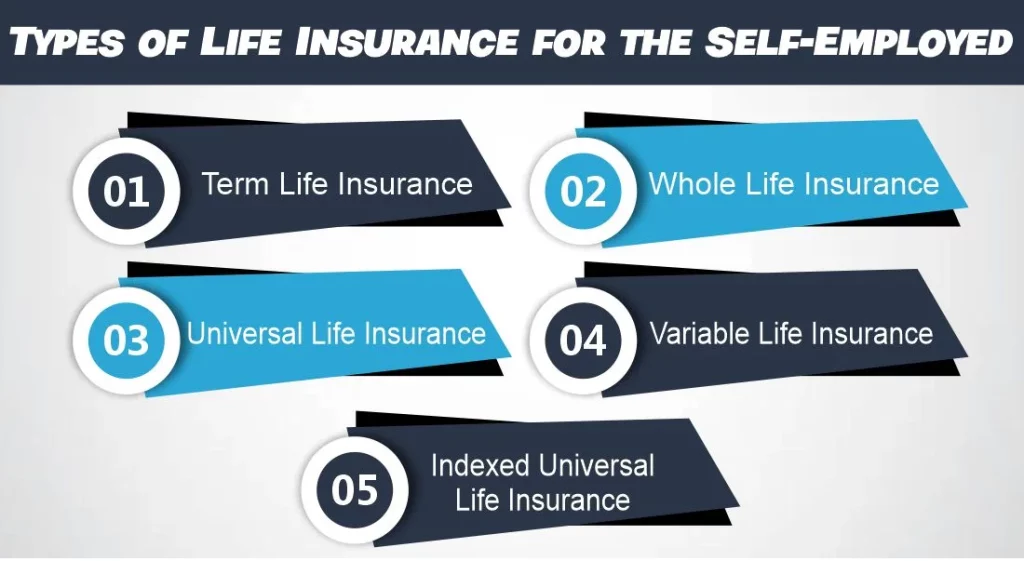

Self-employed individuals have various life insurance options tailored to their specific needs. Here are some common types:

How Much Does Life Isurance Cost?

This policy provides coverage for a specified period, such as 10, 20, or 30 years. If the insured passes away within the policy term, beneficiaries receive the death benefit. It’s relatively affordable and straightforward, offering a fixed premium for the chosen term.

Unlike term life, whole life insurance provides lifelong coverage. It accumulates cash value over time, allowing policyholders to access funds through loans or withdrawals. Premiums typically remain fixed throughout the policy, providing stability but usually at a higher cost than term life.

This policy offers flexibility in premiums and death benefits. Policyholders can adjust the coverage and premium payments according to changing financial circumstances. It also accrues cash value, providing a savings component along with the death benefit.

This type of policy allows the policyholder to invest the cash value portion in various investment options, such as stocks or mutual funds. The policy’s cash value and death benefit fluctuate based on the performance of the chosen investments.

Combining features of universal life and investments tied to stock market indexes, this policy offers potential cash value growth linked to market performance while providing a level of protection against market downturns.

The cost of life insurance for self-employed individuals can vary significantly based on several factors such as age, health, coverage amount, type of policy, and insurer. Here is a tabular representation of potential monthly premiums for different coverage amounts and age groups:

| Age Group | Coverage Amount ($500,000) | Coverage Amount ($1,000,000) | Coverage Amount ($2,000,000) |

| 25-35 | $20 – $50 | $30 – $70 | $50 – $100 |

| 35-45 | $30 – $80 | $50 – $120 | $80 – $160 |

| 45-55 | $60 – $150 | $100 – $220 | $170 – $320 |

| 55-65 | $150 – $400 | $250 – $550 | $400 – $800 |

Please note that these figures are estimates and can vary significantly based on individual circumstances. Factors like health conditions, lifestyle, occupation, and the type of policy can impact the actual cost of life insurance. It’s advisable to obtain personalized quotes from insurance providers to get a more accurate understanding of the costs associated with life insurance for the self-employed.